- +265 (0) 999 970 950 / 951

- mccci@mccci.com

- MCCCI Business Portal

Malawi is a land-locked country in south-eastern Africa, bordered by Mozambique, the United Republic of Tanzania and Zambia. It has a primarily agrarian economy, with 80 percent of the population living in the rural areas. The share of agriculture in GDP has dropped in the last decade from almost 40 percent in 2002 to around the average of 21 percent in recent years. Simultaneously, share of service (in GDP) has been rising to about 55 percent owing to reforms in the financial services sector, a boost in the telecom sector driven by a rise in mobile subscriptions and privatization of the transport sector.

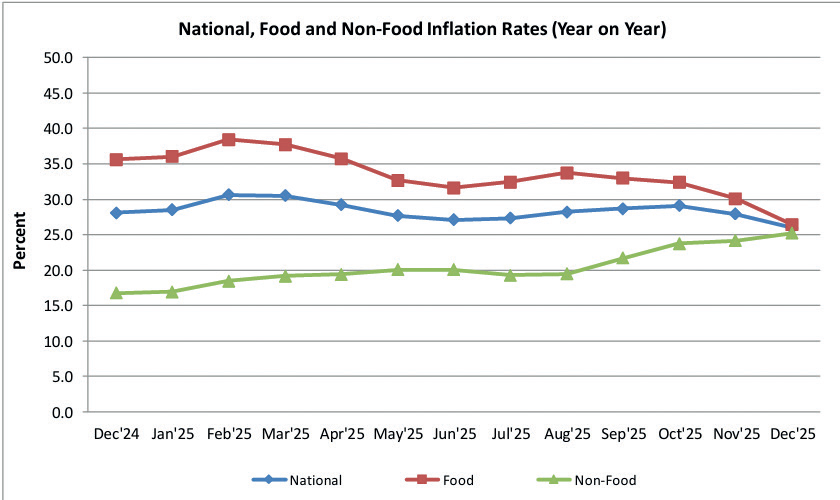

According to the National Statistical Office (NSO), the Year-on-Year inflation rate in Malawi eased to 27.9 percent in November 2025, reflecting a 1.2 percentage point decline from 29.1 percent recorded in October 2025. This moderation in headline inflation was largely driven by a notable slowdown in food inflation, which declined to 30.1 percent from 32.4 percent in the preceding month. The easing in food prices suggests some improvement in domestic food supply conditions, possibly supported by importation of maize, and improved market availability of selected food items

In contrast, non-food inflation increased marginally to 24.2 percent in November 2025 from 23.8 percent in October 2025, indicating persistent price pressures in the non-food category. The uptick in non-food inflation reflects continued cost-push pressures arising from exchange rate depreciation, higher import costs, elevated fuel prices, and increased electricity and transportation charges. Overall, while the decline in headline inflation points to early signs of price stabilization, the divergent trends between food and non-food inflation highlight underlying structural challenges, particularly Malawi’s vulnerability to supply-side shocks and imported inflation, which continue to weigh on the cost of living and business operating costs.

The goods trade balance deteriorated further in October 2025, recording a deficit of US$228.7 million (K400.6 billion), compared to a deficit of US$190.0 million (K333.0 billion) in September 2025. This worsening position was largely driven by a sharp decline in export earnings, which fell by 36.5 percent (US$50.1 million) during the month and was only partially mitigated by a modest 3.5 percent (US$11.4 million) reduction in import payments. Consequently, the October 2025 trade deficit exceeded the US$201.3 million (K352.5 billion) deficit recorded in the corresponding month of the previous year.

Total exports contracted significantly by 36.5 percent, declining to US$87.2 million (K152.6 billion) in October 2025 from US$137.3 million (K240.2 billion) in September 2025. However, export earnings were marginally higher than the US$84.7 million (K148.1 billion) recorded in October 2024. The monthly decline was primarily attributed to weaker tobacco and sugar exports, which decreased to US$55.5 million (K92.7 billion) and US$4.3 million (K7.5 billion), respectively, from US$94.2 million (K164.8 billion) and US$5.3 million (K9.2 billion) in the preceding month.

Imports declined marginally by 3.5 percent to US$315.9 million (K553.2 billion) in October 2025 from US$327.3 million (K573.2 billion) in September 2025, reflecting reduced expenditure on printed books, newspapers and pictures, nuclear reactors and machinery, vehicles, and pharmaceuticals. Despite the month-on-month decline, import payments remained higher than the US$285.9 million (K500.6 billion) recorded in October 2024, underscoring sustained demand for imported goods amid limited domestic substitution.

Overall, the widening trade deficit in October 2025 highlights Malawi’s continued vulnerability to export concentration and seasonal fluctuations, particularly in tobacco, as well as the structural dependence on imports. These trends reinforce the need for export diversification, value addition, and policies aimed at strengthening domestic production capacity to improve the external trade position and ease pressure on foreign exchange reserves.

The Malawi 2063 (MW2063) is Malawi's national vision through which Malawians aspire to transform the country into an inclusively wealthy and self-reliant nation by the year 2063. It is anchored on the three pillars namely; Agricultural Productivity and Commercialization, Industrialization and Urbanization. The MW2063 will be operationalized through four medium term strategies of 10 years each, starting with the MW 2063 First 10-year Implementation Plan (MIP-1) from 2021 to 2030. The MIP-1 is a collection of minimum catalytic interventions that have been determined to contribute to two key milestones of graduating the country to a middle-income status and meeting most of the United Nations Sustainable Development Goals (SDGs) by 2030.

In October 2025, the Malawi kwacha exhibited a mixed performance, recording modest gains against some major currencies while weakening against others, reflecting developments in global financial markets and investor sentiment. Overall, the kwacha remained broadly stable against the United States dollar, closing the month at K1,749.95 per US dollar, supported by ongoing foreign exchange management measures and subdued dollar demand.

Against major European currencies, the kwacha appreciated by 2.1 percent against the British pound and 1.2 percent against the euro, trading at K2,371.39 per pound and K2,078.57 per euro, respectively, at the end of October 2025. The appreciation largely reflected weakness in the pound and the euro, driven by heightened investor concerns over the United Kingdom’s fiscal outlook and skepticism regarding the effectiveness of recent interest rate cuts by the European Central Bank, particularly when compared to the policy stance of the United States Federal Reserve.

In the Asian markets, the kwacha strengthened by 3.8 percent against the Japanese yen, closing the month at K11.25 per yen. The depreciation of the yen was attributed to the widening interest rate differential between Japan and the United States, alongside political uncertainty surrounding the prospect of large-scale fiscal stimulus measures in Japan.

Overall, the mixed exchange rate movements underscore the influence of external monetary policy dynamics and global risk perceptions on Malawi’s exchange rate performance, even as domestic factors continue to shape the kwacha’s stability against the US dollar.

Following a comprehensive assessment of prevailing macroeconomic conditions as at the end of October 2025, the Monetary Policy Committee (MPC) resolved to maintain the Policy Rate at 26.0 percent for the fourth quarter of 2025 (October, November, and December). The Committee also decided to maintain the Lombard Rate at 20 basis points above the Policy Rate, while keeping the Liquidity Reserve Requirement (LRR) ratio unchanged at 10.0 percent for domestic currency deposits and 3.75 percent for foreign currency deposits.

In reaching this decision, the MPC noted that inflation edged up marginally to 28.1 percent in the third quarter of 2025, from 28.0 percent recorded in the previous quarter. The Committee further observed that the inflation projection for 2025 was revised upward to 28.9 percent, compared to 28.5 percent projected at the third MPC meeting, largely reflecting adjustments in pump fuel prices. In addition, the MPC highlighted that limited fiscal consolidation efforts and persistent supply-side constraints continued to exert upward pressure on prices, thereby slowing the pace of disinflation.

The Committee welcomed the Government’s initiative to import maize to address the prevailing food deficit, noting that this intervention is expected to help moderate food inflationary pressures in the near term. However, the MPC emphasized that sustainable disinflation will require deliberate and sustained fiscal consolidation, complemented by broader supply-side interventions aimed at easing structural bottlenecks. Such coordinated efforts by relevant stakeholders are crucial to reinforcing macroeconomic stability and fostering a durable economic recovery.

The equities market recorded moderated trading activity in November 2025, with a total of 23.35 million shares exchanged at a total market value of US$9.32 million across 4,360 trades. This represented a notable decline compared to October 2025, when 38.83 million shares were traded at a value of US$15.89 million through 5,462 trades. Consequently, market activity declined by 39.85 percent in terms of share volume and 41.36 percent in terms of value traded on a month-on-month basis, reflecting subdued investor participation.

Despite the slowdown in trading activity, the market registered positive performance in prices, as evidenced by the upward movement of the Malawi All Share Index (MASI), which rose from 602,600.89 points in October 2025 to 619,709.36 points in November 2025. This translated into a month-on-month return of 2.84 percent, suggesting improved investor sentiment and price gains in selected counters, possibly driven by portfolio rebalancing and inflation-hedging behavior amid prevailing macroeconomic conditions.

Overall, the divergence between lower trading volumes and a rising market index indicates a price-led market performance, where gains were supported more by valuation adjustments than by broad-based increases in market participation.

The unemployment rate in Malawi decreased to 5.60 percent in 2022 from 5.70 percent in 2021. The unemployment rate in Malawi averaged 4.99 percent from 1991 until 2022, reaching an all-time high of 5.70 percent in 2020 and a record low of 4.80 percent in 1991. The top three sectors that employ more people are agriculture, forestry, and fishing, construction and transportation and storage according to NSO 2018.

Real GDP for 2025 is projected to grow by 2.7

percent, slightly below the earlier forecast

of 2.8 percent. This modest downward

revision reflects weaker-than-anticipated

performance across several key sectors,

including manufacturing (1.8 percent),

wholesale and retail trade (0.1 percent),

mining and quarrying (5.3 percent), and

transportation and storage services (3

percent). The subdued sectoral performance

is largely attributed to persistent foreign

exchange shortages, which continue to

limit the importation of raw materials,

intermediate goods, and essential services,

thereby constraining production capacity.

Adding {{itemName}} to cart

Added {{itemName}} to cart